")

{kind=link}

JHVEPhoto

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Cestrian Capital Research, Inc., its employees, agents or affiliates, including the author of this note, or related persons, may have a position in any stocks, security, or financial instrument referenced in this note. Any opinions, analyses, or probabilities expressed in this note are those of the author as of the note’s date of publication and are subject to change without notice. Companies referenced in this note or their employees or affiliates may be customers of Cestrian Capital Research, Inc. Cestrian Capital Research, Inc. values both its independence and transparency and does not believe that this presents a material potential conflict of interest or impacts the content of its research or publications.

Never Mind The Growth, Look At The Cashflow!

We’ve written Qualcomm (NASDAQ:QCOM) stock up three times on these pages of late. Here’s how those calls went so far.

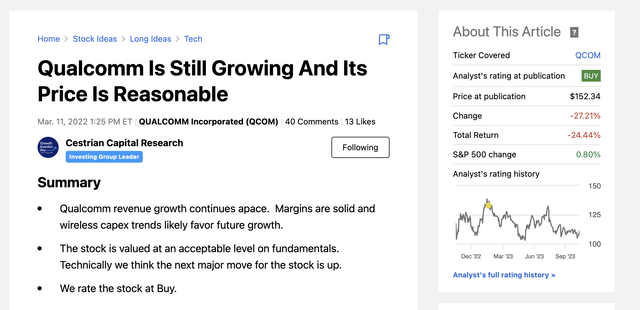

March 2022 – A Stink Buy

QCOM Article I (Seeking Alpha, Cestrian Capital Research, Inc)

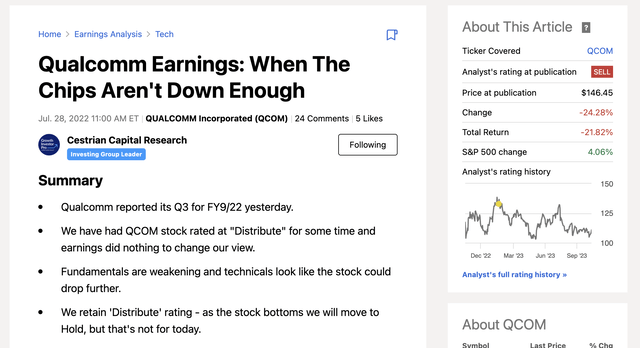

July 2022 – A Righteous Sell

QCOM Article II (Seeking Alpha, Cestrian Capital Research, Inc)

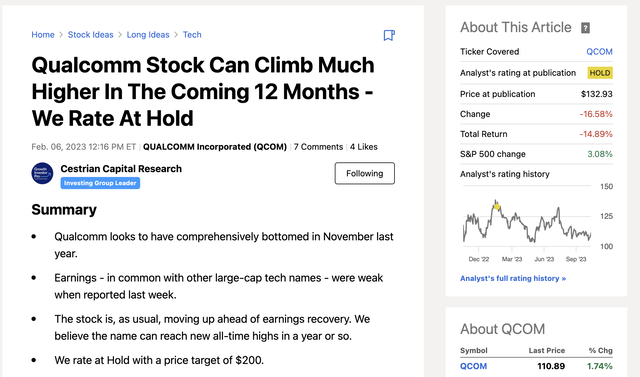

February 2023 – A Thus-Far Unsuccessful Hold

QCOM Article III (Seeking Alpha, Cestrian Capital Research, Inc)

If for some reason you had decided to hang on our every word and do exactly as those notes suggested with no modification or tradecraft on your part (always unwise), thus far you would have lost 24% buying the thing in March 2022, gained 24% shorting the name in July 2022, and lost 15% had you simply held it from February. So let’s call the first two a wash and consider this a 15% net stink call thus far. Not our finest hour, but 15% isn’t irrecoverable in this name in our view.

The company reported its Q4 of FY9/23 Wednesday after the close. So where does it stand now?

Well, we believe it to be buy-able and we rate the stock at Accumulate. And here’s why.

Qualcomm Stock – Fundamental Analysis And Valuation

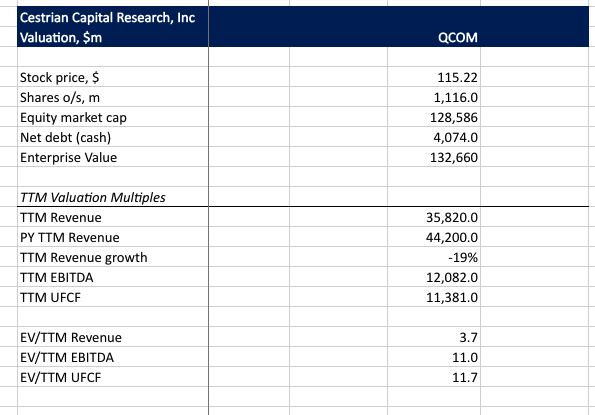

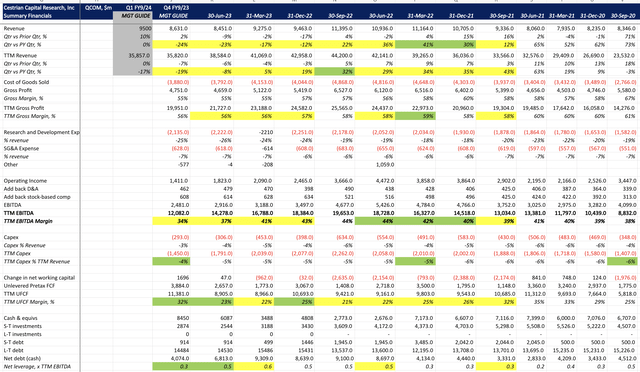

Here are the numbers up to and including this quarter just printed.

QCOM Fundamentals (Company SEC Filings, YCharts.com, Cestrian Analysis)

Revenue isn’t pretty – still in decline (-24% this quarter, and -19% on a TTM basis). And accounting earnings, which we measure using EBITDA, also aren’t so hot. TTM EBITDA of $12bn is way down from the recent TTM high of $20bn struck as recently as the September 2022 quarter.

Where things get more interesting is cash flow, leverage, and valuation multiples.

TTM unlevered pretax free cash flow stands at $11.4bn right now, which (1) is more or less the same as EBITDA, telling you that the EBITDA is high quality earnings, and (2) a recent high – only the June 2021 quarter came close to that mark.

As a result of all this cash generation, net leverage now sits at just 0.3x TTM EBITDA, down from 0.6x only two quarters back.

And valuation sits at just 11.7x TTM UFCF, 11.0x TTM EBITDA or 3.7x TTM revenue. They aren’t big multiples.